Event learnings and takeaways

Webinar recap: What’s next for FDI?

FDI experts, Glenn Barklie, Head of Economic Analysis and Insights, and Matt Harvey, Senior Consultant at fDi Strategies, summarise FT Locations’ webinar, which explored the key FDI trends shaping 2025 and what they mean for 2026.

- March 24, 2026

-

By Glenn Barklie and Matt Harvey

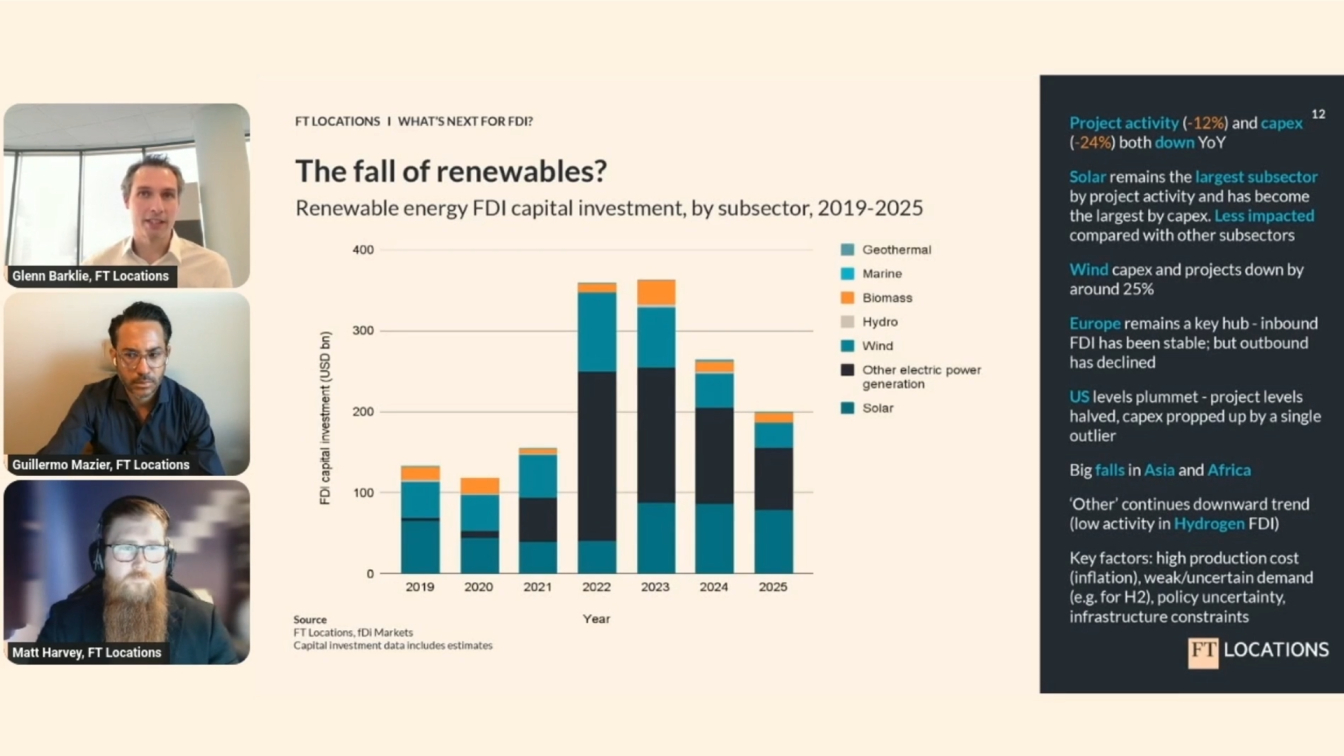

Glenn, Guillermo and Matt presenting on “What’s next for FDI?” webinar

On 20 March, FT Locations’ FDI experts, Guillermo Mazier, Glenn Barklie, and Matt Harvey presented the latest FDI data trends from 2025 and provided strategic insight into what this could mean for locations in 2026.

Watch the webinar on demand: What’s next for FDI?

Key findings

- FDI patterns are shifting

- Data centre investment surges

- Renewable energy investment stalling

- Strategically sensitive FDI on the rise

- Murky outlook for FDI in 2026

- FDI entering a new phase of reconfiguration rather than deglobalisation

- FDI strategies likely to be re-evaluated in 2026

- Business retention and expansion activities expected to see an increased focus

- Capacity building and training continues to be prioritised

FDI at a crossroads: shifting patterns, sectors and geopolitics in 2025

Global greenfield foreign direct investment (FDI) entered a pivotal phase in 2025, marked by diverging trends, evolving sector priorities and growing geopolitical influence. For the first time since 2020, greenfield FDI project activity declined, falling by 6.6% – a drop that aligned closely with our forecasts produced last year. Yet this slowdown in activity was offset by a modest 3% rise in announced capital investment (capex). These trends point to the changing nature of FDI, with both sectoral and geographic shifts. The divergence between project numbers and capital expenditure also highlights a shift in the scale of FDI. Fewer projects are being announced, but they are, on average, larger and more capital-intensive.

Greenfield FDI project numbers falling in 2025 while total capital investment continues to rise.

Regionally, the picture is mixed. Western Europe retained its position as the leading destination region for project activity and the third largest for capital investment. While project numbers have declined for three consecutive years, capex reached a new peak, suggesting a concentration of capital into fewer, larger initiatives.

A similar pattern emerged in North America, where project activity fell by 7% from its 2024 peak, yet capital investment surged. In contrast, Asia, the largest market for FDI by capital, saw both project numbers and capital investment fall in unison by 12%. Conversely, the Middle East stood out as the leading growth region, with capital investment rising by 73% and project activity increasing by 14%. Yet ongoing geopolitical tensions are likely to disrupt this trajectory.

Elsewhere, challenges persist. Emerging Europe continues to experience a sustained decline in both project activity and capital investment, while Latin America and Africa saw modest gains in project numbers but sharp drops in capital expenditure.

Sector shifts reshape the FDI landscape

At a sector level, the composition of FDI is changing rapidly. Communications emerged as the leading sector by capital investment in 2025, overtaking renewable energy. The capital investment growth in communications is primarily driven by large-scale data centre projects, which have become increasingly central to global investment strategies. The number of ‘megaprojects’ (those valued at $1bn+) in the communications sector rose significantly in 2025. More broadly, communications, semiconductors and renewable energy were the top sectors for megaprojects in 2025. This marks a notable shift from 2019, when megaproject investment was dominated by coal, oil and gas, alongside chemicals and renewables. The transition underscores how digital infrastructure and advanced manufacturing are reshaping global investment priorities.

However, sector performance remains uneven. Only half of all FDI sectors recorded growth in capital investment in 2025, and just a third saw increases in project activity. Some niche sectors posted outsized gains. Two billion-dollar-plus investments in the US shipbuilding industry drove up capital investment levels in the non-automotive OEM sector by 284%. Meanwhile, the doubling of FDI capex in the engines and turbines sector was driven more by an increase in project activity than a single capex outlier. And the space and defence sector reached record highs in 2025 by both project activity and capital investment. Conversely, automotive FDI declined amid weakening demand for electric vehicles, and electronic components saw a downturn (-49%).

Thematic drivers: AI, defence and strategic resources

Beyond sectors, broader themes are increasingly shaping FDI flows. Artificial intelligence (AI) has become the dominant investment theme, with project numbers rising by 51% year-on-year. AI investment is no longer confined to software and IT services. Whereas nearly 90% of AI-related projects were concentrated in that sector in 2019, the share has fallen to 65% in 2025 as AI-related FDI was spread across 25 different sectors.

We are also seeing the continued rise of defence-related FDI themes. Military tech has been growing since 2022, the year Russia invaded Ukraine. And although drones can include other sectors, for example food delivery or crop monitoring, the majority of FDI is linked to the space & defence sector. And there is significant overlap with military technologies. At the same time, investment in critical minerals – essential for semiconductors and infrastructure – is gaining momentum, reflecting supply chain concerns and resource security priorities.

There are also early signs that tariffs and trade barriers are beginning to influence investment decisions, a trend expected to grow in the coming years.

The data centre boom accelerates

One of the clearest manifestations of these trends is the rapid expansion of data centre-related FDI. In 2025, both project activity and capital investment reached new highs, with average project values increasing from $250m in 2019 to $1bn. This growth is closely tied to rising demand for AI and digital services, as well as forecasts of global data centre capacity reaching 200GW by 2030.

Data centre FDI is also becoming more geographically diverse, spanning 41 destination countries in 2025 compared with 28 in 2019. While the US remains the dominant source of investment, countries such as the UAE and China are playing a growing role through major joint ventures. However, the strategic importance of data centres introduces new risks, as they increasingly become targets in geopolitical conflicts.

Renewables pause, strategic sectors rise

In contrast, renewable energy FDI has entered a period of slowdown. Both project activity and capital investment declined for a second consecutive year, with wind and hydrogen projects particularly affected by cost inflation, policy uncertainty and infrastructure constraints. Solar energy has proven more resilient, remaining the largest subsector by project numbers and becoming the largest by capital investment for the first time in seven years.

Data centre FDI is also becoming more geographically diverse, spanning 41 destination countries in 2025 compared with 28 in 2019. While the US remains the dominant source of investment, countries such as the UAE and China are playing a growing role through major joint ventures. However, the strategic importance of data centres introduces new risks, as they increasingly become targets in geopolitical conflicts.At the same time, investment in strategically sensitive industries is surging. These sectors, including, but not limited to, communications infrastructure, critical minerals, defence and energy, now account for roughly one-third of all FDI projects and three-quarters of total capital investment, equivalent to over $1tn in 2025. This reflects a growing emphasis on national security and economic resilience in investment decisions.

Share of global FDI flowing into strategically sensitive sectors has increased since 2016, with capital investment rising more sharply than project activity.

A more fragmented global landscape

Underlying these trends is a broader geopolitical shift. Analysis of global investment flows suggests that FDI is increasingly aligning along geopolitical blocs. Countries more aligned with the US accounted for around two-thirds of global FDI capital in 2025, up from 47% in 2015. In contrast, the share of FDI flowing into China-aligned countries has declined from a high of 29% in 2016 to 10% in 2025.

This fragmentation suggests that investment decisions are increasingly influenced by strategic considerations such as political alignment, supply chain security and economic partnerships rather than purely market fundamentals.

Outlook for 2026: complexity and competition

Looking ahead, FDI is entering a more complex and fragmented phase. Early indicators point to a further slowdown in 2026, with provisional project activity data down by 15% in the first couple of months. Geopolitical tensions, particularly in the Middle East, are likely to weigh on investment flows, while creating opportunities for alternative destinations such as Southeast Asia, India, North Africa and Eastern Europe.

Competitiveness is also evolving. Investors are placing greater emphasis on stability, security and resilience, potentially favouring “resilience-seeking” investment over traditional efficiency-driven models. At the same time, rising trade tensions and tariffs are expected to play a more prominent role in shaping global investment patterns in the coming years.

In summary, 2026 marks a turning point for FDI. While FDI capital continues to flow, it is doing so in new ways – across different sectors, regions and strategic priorities. This signals a reconfiguration of the global investment landscape rather than a retreat from globalisation.

So what does this mean for IPA and EDOs? In 2026 priorities may include:

Re-evaluating sector and target market strategies

In 2026, many IPAs and EDOs are expected to revisit their FDI strategies. This includes sharpening their focus on priority sectors and target markets, as competition intensifies and global investment patterns shift.

Sector strategies are likely to become more targeted. Greater emphasis will fall on high-value and contestable sectors, including in strategically sensitive sectors such as data centres, semiconductors and communications.

At the same time, organisations are expected to reassess which source markets to prioritise. We expect the focus will be on markets that align closely with local strengths within priority sectors and subsectors identified , with IPAs continuing to develop clear positioning statements and sector and market specific narratives that will resonate with investors in priority markets.

Focus on aftercare activity

Aftercare and business retention and expansion (BRE) activity is expected to see an increased focus from global IPAs and EDOs. Ongoing geopolitical tensions and supply chain pressures are increasing uncertainty, making investor retention and expansion more important.

A structured aftercare approach helps organisations identify reinvestment opportunities by addressing investor concerns early. Many of these concerns such as operating conditions, regulatory clarity and risk assessments, are key business environment factors often being explored by potential firms exploring locations for future investment projects.

Clear engagement frameworks and approaches, supported by practical tools such as well-designed CRM systems, enable more consistent and proactive investor aftercare. This, in turn, can strengthen investor confidence and support long-term growth opportunities. We see this being a key operational area IPAs and EDOs will aim to strengthen as we move through 2026.

Skills development to ensure readiness to attract FDI in 2026

Strengthening organisational capacity will be critical to delivering an effective FDI strategy in an increasingly competitive environment. As competition increases for a smaller pool of potential investment projects, IPAs and EDOs need to ensure that they have the skills in-house that are required to secure investments.

Many organisations are reviewing skills gaps and investing in targeted training in a wide range of areas, from investment attraction and lead generation through to investor aftercare and in more specific areas such as small or rural community economic development or commercial approaches to FDI.

We see this focus on internal capacity building being likely to continue in 2026 and beyond as organisations ensure that not only their location is investment ready, but that their teams are fully equipped to support prospective investor clients.

All in all, IPAs and EDOs must be prepared for a new phase of FDI, one in which the most agile and equipped agencies are the ones most likely to succeed.

What’s next for FDI? Watch the full webinar on demand

Further reading

Read blog: The new FDI map - the rise of investment blocs in a fragmenting world

Read blog: Targeting investors and markets in a multipolar world

Turn global investment data into trusted insight with fDi Markets

Strengthen your investment strategy with fDi Strategies

Compare locations with intelligence that drives better decisions using fDi Benchmark

Learn more about FT Locations

FT Locations is the world's most comprehensive and trusted provider of investment promotion and economic development data and digital solutions for the foreign and domestic direct investment industry.