Thought leadership

Redirection, not retreat: Tariffs and North American FDI

US tariffs have disrupted North America’s investment landscape without cutting overall investment into Canada and Mexico, where levels remain broadly stable. Instead, the uncertainty is shifting where companies put their money, with more flowing into the US as businesses adjust supply chains to avoid extra costs. At the same time, Canada and Mexico are attracting a wider mix of investors from Europe and Asia, gradually reducing their reliance on the US.

- April 23, 2026

-

By Jordan Fox

The impact of Tariffs on North American FDI

Canada and Mexico were among the countries most adversely hit by US President Trump’s tariffs in 2025. US tariff policy was marked by threats, delays, exemptions, and partial rollbacks with rates ranging between 10 and 35 per cent, often varying by product area or abrupt shifts in approach.

However, under the United States-Mexico-Canada Agreement (USMCA), a majority of Canada and Mexico’s trade with the US remained exempt from tariffs, around 90 per cent and 84 per cent, respectively. Yet, while strategic industries such as energy and critical minerals largely dodged tariffs under USMCA standards, others, including automotives and consumer goods, were more exposed.

Recent developments have only deepened investor uncertainty in the region. In February 2026, the US Supreme Court ruled against President Trump’s use of the International Emergency Economic Powers Act (IEEPA). The Trump administration responded to the ruling with a 15 per cent tariff rise, further demonstrating the fragility of existing trade arrangements and the volatility of the North American market.

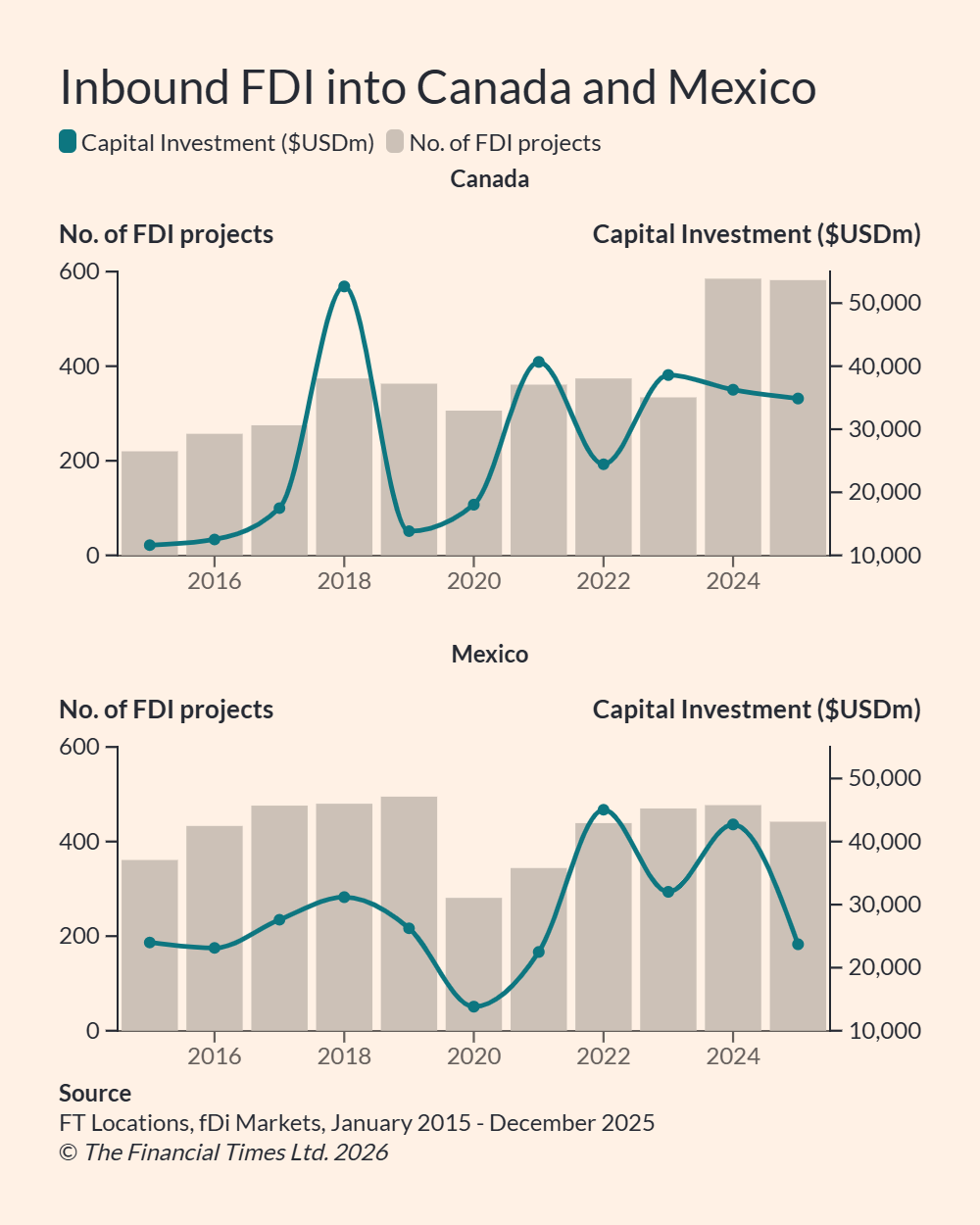

Despite these pressures, data from fDi Markets show that greenfield FDI figures in Canada and Mexico remained steady in 2025. Project announcements and capital investment stayed consistent with levels from previous years, apart from a dip in capital investment into Mexico.

FDI into Canada and Mexico remains broadly stable despite tariff volatility

In 2025, foreign companies announced 582 FDI projects in Canada. It stands at a similar level to the 585 projects in 2024, following a dramatic rise from 334 projects in 2023. Capital investment also held steady, declining slightly by 3 per cent from an estimated $36.3bn in 2024 to $34.9bn in 2025.

Mexico saw a more pronounced decline in capital investment, with foreign companies announcing an estimated $23.7bn worth of investments in 2025, the country’s lowest recorded figure since 2021. Project announcements also dropped slightly to 442, down from 477 in 2024, but remained broadly in line with figures over the past decade.

In comparison, US inbound capital investment FDI hit record levels, standing at $321.2bn in 2025. Project announcements stood at 2,059, a level exceeded only by a peak of 2,259 in 2024.

Tariffs drive shift in investment and supply chains

Tariffs have prompted foreign companies to redirect investment in North America, drawing them directly towards the US market. This is already taking shape in the case of Stellantis’s $13bn investment to relocate operations from Ontario to Illinois and General Motors’s $4bn plan to shift 300,000 units of production capacity from Mexico to the US by 2027.

At the same time, companies are also seeking to avoid the burden of additional duties by nearshoring and offshoring operations elsewhere. For example, Chinese EV makers, a primary target of President Trump’s tariffs, have faced heavy 100 per cent duties dating back to the Biden administration. As a result, companies such as BYD have turned to Mexico as their alternative operations base in North America. The company is also considering establishing local operations in Canada after tariffs on 49,000 Chinese EVs were slashed from 100 to 6.1 per cent early this year.

Others are restructuring operations further afield. Canada-based Bittele Electronics, which specialises in low-volume printed circuit board (PCB) manufacturing, opened a new assembly and manufacturing facility in Seberang Perai, Malaysia. The facility provides a manufacturing option to its customers in the US market, which avoids tariffs on components produced in Canada and China.

Canadian Prime Minister, Mark Carney during his speech at the World Economic Forum in Davos, Switzerland © Krisztian Bocsi/Bloomberg

The volatile state of US tariff policy has heightened concerns over economic coercion. Against this backdrop, Canada’s Prime Minister Mark Carney argued at the World Economic Forum in Davos that middle powers must confront the decline of a rules-based order and recognise a new reality, one dictated by hegemony. Carney urged that diversification was essential, warning that “If we’re not at the table, we’re on the menu.”

FDI sources diversify as US share declines

Even so, the US remains the leading FDI source market for Canada and Mexico. Over the past decade, the US was the source of as much as 51 per cent of inbound FDI projects in Canada and 40 per cent in Mexico. However, recent figures suggest that the US share of FDI projects is declining as other source markets pick up, signalling that diversification may already be underway.

US remains the dominant FDI source, but tariffs are driving greater diversification across North America.

This shift was identified when Canada saw a surge in inbound FDI projects in 2024, particularly drawing investment into service-based sectors, including business and software IT services. Despite an increase in total project numbers, growth in announced projects from the US lagged behind other source markets, leading to a decline in its project share from an average of 45.8 per cent between 2015 and 2023 to 38.3 per cent between 2024 and 2025.

Alternatively, Western European countries, such as the UK, France, and Germany, have boosted project numbers in Canada. UK-based companies, for example, recorded an average of 54 projects in 2024 and 2025, up from an average of 30 projects between 2015 and 2023. Investment from Asia-Pacific countries, including Japan, India, China, and Australia, has also gained momentum. For instance, FDI project activity from Japan has jumped from an average of 9 projects between 2015 and 2023 to an average of 24 projects between 2024 and 2025.

A similar deceleration in US-sourced projects is noted in Mexico. The US remains Mexico’s largest source market, but its project share has continued to decline in recent years. In 2025, it represented 30.1 per cent of inbound FDI projects in Mexico, falling among some of its lowest shares over the past decade.

By contrast, a surge in investment by Chinese companies since 2023 has strengthened China’s position as a key source of FDI into Mexico. In 2025, China recorded a peak of 49 projects in Mexico, largely targeting manufacturing sectors such as automotive components and industrial equipment.

FDI holds steady but what’s next for the US?

While the US holds its status as the largest source of FDI for its neighbours, the data shows that Canada and Mexico are beginning to attract FDI from a broader range of source markets, a trend that started before President Trump’s Liberation Day. Tariffs have not destabilised overall FDI project numbers or capital investment for North America, but their volatile nature has amplified investor uncertainty and strained traditional trading relationships. The question now is whether continued turbulence in tariff policy will further expedite diversification efforts from Canada and Mexico.

Further reading

Stellantis’s $13bn investment to relocate operations from Ontario to Illinois

General Motors’s $4bn plan to shift production from Mexico to the US

Chinese EV makers face heightened tariffs

Davos 2026: Special address by Mark Carney, Prime Minister of Canada

Join the global network that trusts fDi Markets to navigate greenfield investment with confidence.

Read blog: One year on since Liberation Day: Tariffs, tantrums and FDI

Read blog: If investors can’t use your data, they won’t choose your location

Learn more about FT Locations

FT Locations is the world's most comprehensive and trusted provider of investment promotion and economic development data and digital solutions for the foreign and domestic direct investment industry.