Thought leadership

One year on since Liberation Day: Tariffs, tantrums and FDI

One year after “Liberation Day”, US tariffs have introduced volatility into global trade but have yet to significantly reshape foreign direct investment patterns. While the US economy remains relatively resilient, signs of strain are emerging, including higher inflation and a softer labour market. Despite policy uncertainty, the US remains an attractive place for businesses to invest, supported by its strong economic fundamentals.

- April 16, 2026

-

By Glenn Barklie

One year on since Liberation Day

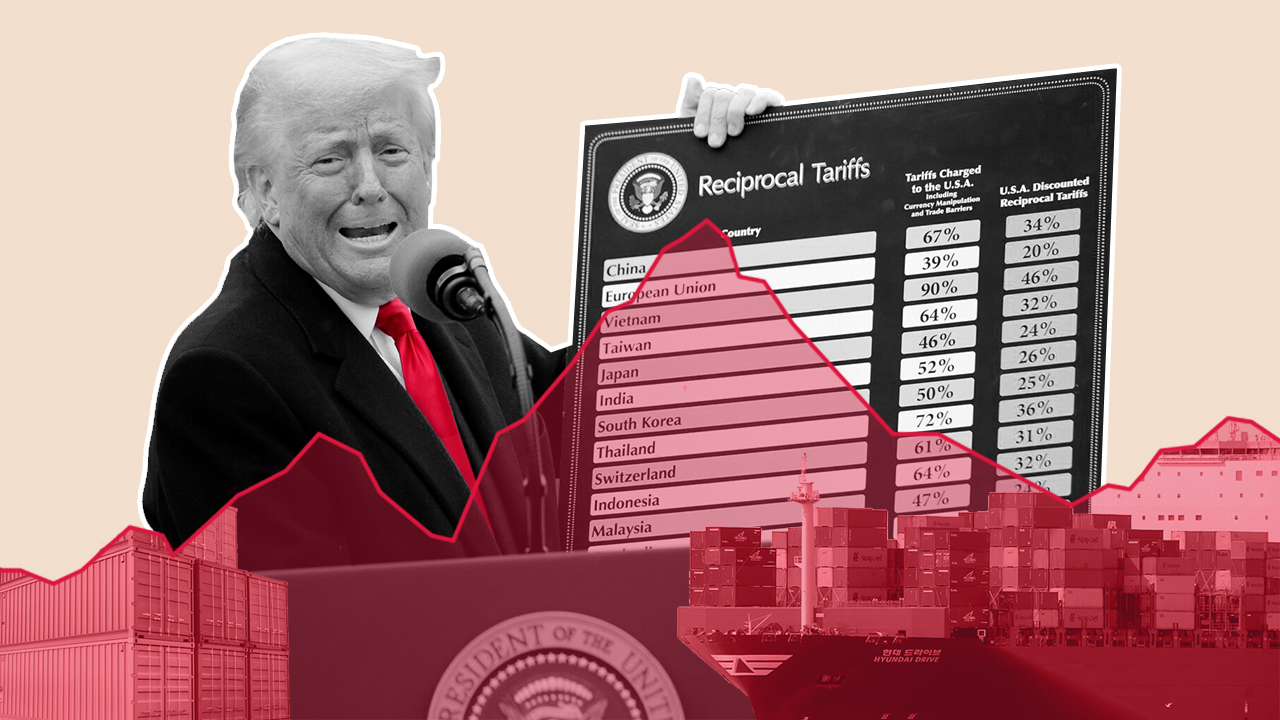

On 2nd April 2025, President Trump announced a sweeping package of tariffs – dubbed ‘Liberation Day’ – aimed at reshaping global trade. The idea is relatively simple. Trump believes that the US trade deficit (in goods) is too large – i.e. the US is importing far more goods than it is exporting. This much is certainly true. At the time of his Liberation Day speech, the overall trade balance stood at -$60.1bn in April, 2025. Although services posted a surplus of $26.4bn, this was outweighed by a goods deficit of $86.5bn.

The US has the largest trade deficit in the world, but it is falling

Making America Great Again

Trump argues that high import levels are harming US competitiveness. His tariff plan had a couple of primary objectives: price out cheap imports so that US companies become more competitive by default; and/or entice foreign companies and US companies with foreign operations to establish facilities in the US – creating local jobs and growing domestic industries, as well as ensuring the US remains the key market for innovation.

Trump started by implementing an array of varying rates by country and product area. Again, the formula was relatively simple – countries with larger trade surpluses with the US faced higher rates. However, on 20th February 2026, the US Supreme Court ruled that the tariffs were unlawful. On that same day the administration imposed a 10 per cent tariff on countries as per Section 122 of the Trade Act of 1974. This can last for 150 days. This has meant that Vietnam, for example, has had its tariff rate change from 46 per cent to 20 per cent to 10 per cent, all in a few months. Additional measures still apply to certain countries, including China and Canada, depending on the goods involved.

How has the US performed in the last year?

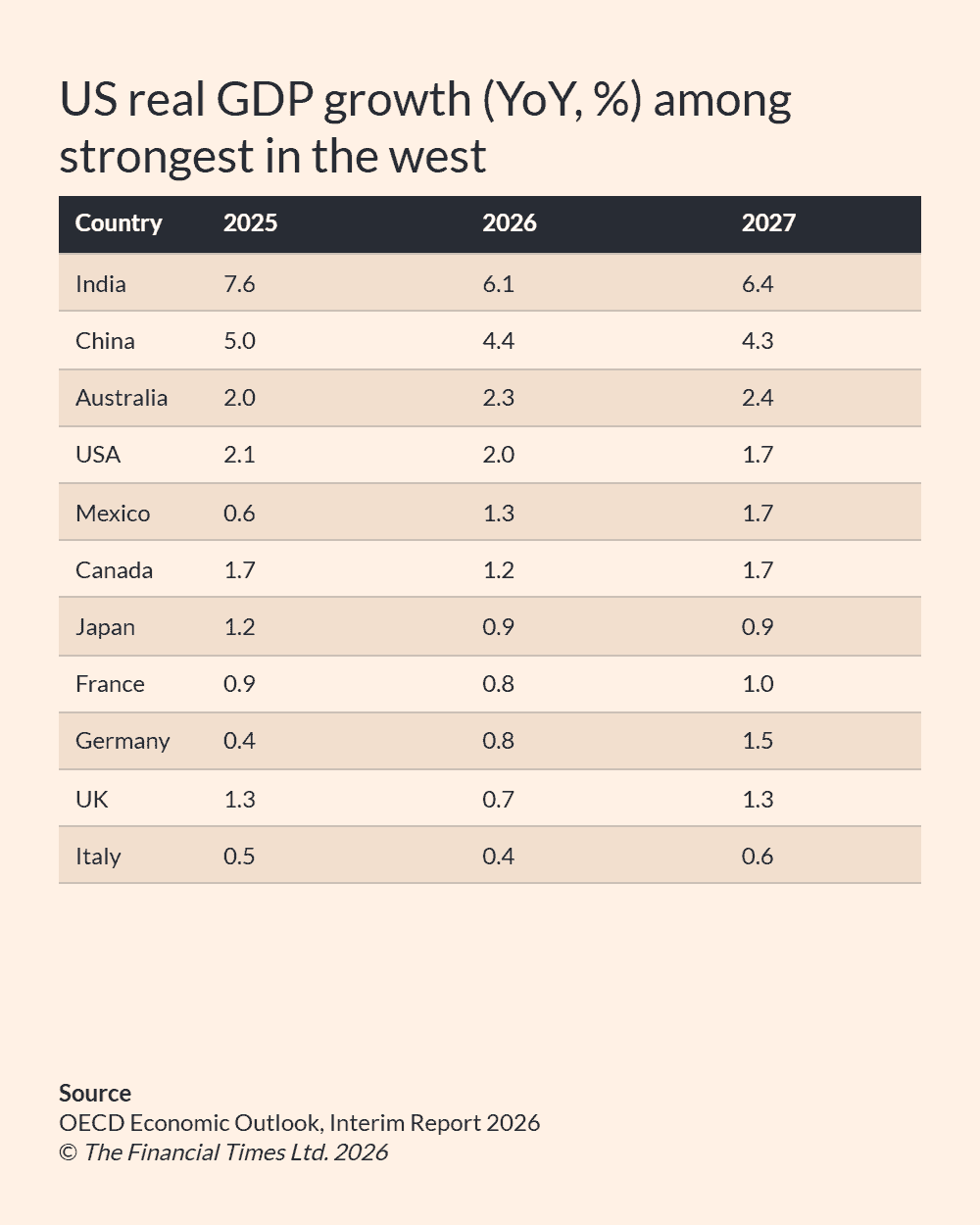

US economic growth has remained relatively resilient. In 2025, real GDP growth was 2.1 per cent according to the US Bureau of Economic Analysis. This was the country’s lowest increase in five years, partly due to a slowdown in the labour market and delayed activity due to tariffs. Even so, the US outperformed many other large economies.

The OECD expects global growth in 2026 to be supported by momentum in technology and lower-than-anticipated tariff rates as well as building on a solid 2025. Yet the conflict in the Middle East is driving up energy prices and disrupting supply chains across a range of industries, which will impact growth. Current projections assume these disruptions are temporary.

Among major economies, only India, China and Australia are projected to record stronger growth than the US in 2026.

Meanwhile unemployment in the US has edged up slightly. In February 2026, 4.4 per cent of the labour force were without a job. While still low in historical terms, it does indicate a slight softening of the labour market.

Inflationary pressures remain more pronounced in the US than in several peers. The OECD estimates that inflation in the US will be 4.4 per cent in 2026, compared with 4 per cent in the UK, 2.9 per cent in Germany and 2.4 per cent in Canada. Strong demand, rising wages and services (particularly housing) are expected to drive up price levels.

The dollar has weakened since the start of Trump’s second term, reflecting policy uncertainty, expectations of rate cuts, trade tensions and rising government debt. For example, both the Sterling and Euro have strengthened against the dollar. Sterling has strengthened from $1.27 at the end of 2024 to $1.34 in March 2026, while the euro has risen from $1.08 to $1.17. Despite this, the greenback remains strong by longer-term standards.

Impact on FDI

The US’ FDI performance has been strong since Covid-19 caused levels of both the number of FDI projects and amount of FDI capital investment to plummet in 2020. In 2024, the number of inbound FDI projects peaked (2,261), while inbound announced FDI capital investment peaked in 2025 ($321 bn). In fact, inbound FDI capex grew by a further 33 per cent in 2025 - driven by megaproject investments - i.e. those valued at $1bn+. Not only did the number of such projects increase but the amount of capital being invested rose more sharply. In 2025, these megaprojects accounted for almost two-thirds (61 per cent) of the total announced FDI capital investment into the US. Semiconductors, data centres, energy and metals sectors saw the largest FDI capital investment announcements into the country. FDI job creation has also been on a generally positive trend. In 2025, FDI job creation is estimated to have exceeded 255,000, up 5 per cent on the previous year.

How much is tariff-driven?

So far, tariffs appear to have had a limited direct impact on FDI decisions. Most companies adopted a wait-and-see mentality. There were, however, some companies that made announcements to limit the impact of any potential tariffs.

For example, Stellantis announced plans to relocate its production of the Jeep Compass and Cherokee vehicles from Ontario, Canada to a reopened assembly plant in Belvidere, Illinois. The facility, which has been closed since 2023, will receive an investment of $600m. Once operational in 2027, it will serve the US market and create 3300 jobs. The project forms part of the company’s plan to invest $13bn by 2029 to increase its US production capacity and mitigate the effect of President Trump’s tariffs on the automotive industry.

Other companies expanding their US presence include JCB, GE Appliances and Gerdau.

At the same time, some businesses are restructuring operations outside the US For example, Canada-based Bittele Electronics, which specialises in low-volume printed circuit board (PCB) manufacturing, opened a new PCB assembly and electronics manufacturing facility in Seberang Perai, Malaysia. The facility will serve global clients, especially the US market. The company highlighted that US clients now have a manufacturing option unaffected by recent tariffs on goods from Canada and China.

There are also examples of US companies that have established abroad due to or in spite of the rise in tariffs. For example, illumiPure, a US-based LED lighting company, announced plans to open a manufacturing facility in Dubai. The company cited US tariffs as a reason for setting up manufacturing operations abroad. It will be the company’s first international expansion.

Conclusion

One year on from Liberation Day and the impact of tariffs on FDI are (so far) relatively muted. However, greenfield investments into the US remain at an elevated level by project activity, whilst the amount of FDI capital being invested has reached an all-time high. There is clear alignment in inbound investment in strategically sensitive sectors such as semiconductors and energy. Yet only a small number of FDI projects have cited tariffs as a key driver of the project decision. However, that’s not to say that other projects are happening without considering tariffs as a (key) component. Also, I do expect the impact of tariffs to be more prevalent over the next couple of years – as the time from FDI decision to ribbon-cutting realisation can be anywhere between one to five years, depending on the industry.

Economically, the US has continued to be in a position of strength. Yet there are some soft signs – elevated inflation, slowing economic growth, labour market softening and a continued weakened dollar – that policy uncertainty is having a more negative than positive impact. The prolonging of the war in the Middle East will also have negative impacts on global markets, including the US.

Even so, the underlying structural advantages that the US possesses continues to make it an attractive investment destination.

Further reading

Go beyond the headlines with the global database tracking greenfield investment

Read blog: If investors can’t use your data, they won’t choose your location

Compare locations with intelligence that drives better decisions using fDi Benchmark

Read blog: Webinar recap: What’s next for FDI?

Transform your website with data visualisation today using ZoomProspector

Read blog: The new FDI map - the rise of investment blocs in a fragmenting world

Learn more about FT Locations

FT Locations is the world's most comprehensive and trusted provider of investment promotion and economic development data and digital solutions for the foreign and domestic direct investment industry.