Thought leadership

FDI data trends of 2025

A month-by-month look back at the most interesting trends discovered by our data tools throughout 2025. Along with these trends, Glenn offers expert early predictions on what could shape markets in 2026.

- December 04, 2025

-

By Glenn Barklie

Throughout the year we have provided subscribers of our products with monthly updates, covering some of the most interesting trends in foreign direct investment (FDI), discovered through our data tools.

Now, we’re offering a preview. Get the highlights in our fortnightly email with your free Knowledge Hub registration — Sign up now

In this article, I review each trend we identified in 2025, how it evolved, and what it might signal for 2026.

JANUARY

Saudi Arabia to rival UAE for headquarter FDI?

We kicked off the year examining the rise in FDI into Saudi Arabia. Specifically, we analysed foreign companies opening headquarter operations in the Middle East. Driven by a dedicated programme to attract regional headquarters, Saudi Arabia also introduced a legal requirement (in many cases) that required a company to open a regional headquarters to work with state entities. Additionally, the country has several other pull factors enticing foreign investors. Headquarter investments shot up in 2022 and have remained strong, with headquarter activities accounting for around 13.5% of total FDI projects into Saudi Arabia. This compares with around 5% in the UAE. Saudi Arabia has become one of the top five destinations globally for regional headquarter operations FDI. Its rivalry with the UAE is also hotting up. In 2019/20, Saudi Arabia was only receiving one HQ FDI project for every ten into the UAE. By 2024, it was receiving eight HQ projects for every ten into the UAE.

2026 Outlook: The Middle East will remain a key FDI market as investors seek its high(er) growth potential compared with more mature markets. The UAE and Saudi Arabia will continue to benefit as the two leading economies in the region.

FEBRUARY

US posting record inbound FDI numbers in 2024

In February, we looked back at the success of inbound FDI into the US (pre-Trump tariffs). In 2024, foreign companies created 2,259 FDI projects — the highest of any year on record. However, US outbound FDI continued to show signs of falling levels. While inbound projects were 16% higher in 2024 compared with 2019, outbound US FDI project volumes were 20% lower.

Data shows FDI project activity and capital investment into the US reached a new peak in 2024

In 2025, we are projecting inbound investment to remain high, around the same levels as those in 2022 and 2023, but below the peak in 2024. However, of note, announced capital investment (excluding generic pledges) FDI in 2025 between January-September (based on latest data available) is already 11% higher than 2024 (full year), pointing to large-scale investments, particularly in data centres, semiconductors and renewable energy.

2026 Outlook: The US will continue to be the leading destination and source market globally for FDI. Domestic protectionist measures may well see the continued decline in outbound US FDI activity as well as the continued focus of tech companies to build infrastructure instead of other types of operations — reducing FDI volumes in software & IT services. In terms of inbound FDI, Trump’s tariffs should have more of an impact in the 2026 numbers compared with 2025.

MARCH

Canada’s record inbound FDI

We continued the theme of record FDI numbers in North America, this time focusing on Canada. In 2024, inbound projects into Canada grew substantially. A trend that is continuing in 2025. Although the US remains Canada’s leading source market for FDI, its dependency is declining. Between 2019 and 2021, US companies accounted for around 47% of total FDI projects into Canada. Since 2022 that proportion has fallen. It currently sits at 39% for 2025 (based on January-September data). This shows that Canada is attracting investments from elsewhere — most notably the UK, France, Switzerland and Germany in Europe and India, Japan, China and Australia in Asia.

2026 Outlook: Canada is one of the most impacted countries of Trump’s tariffs, which could lead to foreign investors reconsidering the country as a viable option. Its economy is also growing slowly. However, service-based FDI, which is less impacted by tariffs, has been key to Canada’s recent growth. All in all, FDI into Canada is unlikely to continue its recent upward boom, but it is likely to remain as one of the key global hubs for foreign companies.

APRIL

The rise of Vietnam

In April, we focused on Vietnam, a key beneficiary of supply chain realignment away from China. Our analysis showed that the sectors driving Vietnam’s growing trade surplus with the US were the same ones attracting higher levels of FDI — pointing to a clear alignment between trade and investment trends. Vietnam’s cost advantage over regional peers has helped underpin this growth and we showcased Vietnam could be around 50% cheaper than China for a 900-person textile manufacturing operation (using analysis from fDi Benchmark). FDI into Vietnam recovered to pre-Covid levels in 2023 and rose further in 2024. However, the pace has slowed in 2025, likely reflecting a mix of investor caution amid US tariff decisions and a broader cooling in Asian and global FDI flows. While fundamentals remain strong, the near-term outlook suggests a period of pause as firms reassess regional exposure and policy risks.

2026 Outlook: Vietnam remains a highly attractive destination for foreign investors, and inflows are likely to recover as global FDI conditions improve. The newly agreed US reciprocal tariff (set at 20%) brings Vietnam broadly in line with regional competitors such as Cambodia and Thailand and remains well below the levels applied to China and India. As a result, the change is unlikely to significantly alter investor sentiment, particularly given that Vietnam’s appeal continues to rest on competitive labour costs, improving infrastructure and its deepening role in global supply chains.

MAY

Megaprojects dominating FDI

Megaprojects: those defined as having an announced capital investment of over $1bn — have been on the rise in recent years. Although the volume of these projects peaked in 2023, there is a notable upward shift in the number of megaprojects since 2022 compared with prior years. The increase of such projects is driving up the average size of FDI projects, for example average project size in 2025 is $86.5m compared with $53.6m in 2019. But it’s not just the fact that there are more of these types of projects, the megaprojects themselves are getting bigger.

2026 Outlook: Megaprojects will continue to uplift FDI capital investment. Data centres will remain the key focus of mega investments with a rise in the number of projects forecasted. A potential rebound in the number of renewable energy projects is also likely and, after a low in 2025. However, semiconductor, coal, oil & gas and automotive sectors are likely to remain lower in volumes. That said, the overall average size of megaprojects is likely to continue to rise.

JUNE

US states using incentives to draw film and media investment

Incentives can be a key hook to attract investment. We have seen a sharp rise in the total value of film production incentives being offered in the US since 2022, particularly in New York and California. Although these incentives were for both foreign and domestic companies, it corroborated the FDI trend of the US being the leading destination market for motion picture & sound recording industries

2026 Outlook: FDI activity likely to remain stable, while incentives for US companies to remain elevated.

JULY

Global military spending increases sees FDI surge

We discovered global military spending hit a record $2.7tn in 2024, as governments responded to deepening conflicts and rising tensions. In turn, we are also seeing record levels of military technology FDI. Whilst the number of military technology FDI projects grew by 29% between 2023 and 2024, 2025 levels will surpass once more, potentially growing by a further 33%. Capital investment FDI in 2025 is already (based on Jan-Sep data) above its full year 2024 level. Although FDI levels are relatively low compared with other sectors, it is certainly an emerging subsector to keep an eye on.

A sharp rise in FDI in global military technology

2026 Outlook: Governments will continue to increase military spending in the short-medium term. This will encourage increased levels of FDI in the subsector. The US, Germany, France and the UK are likely to be key source markets driving the increase in FDI.

AUGUST

Innovation is the key to FDI success?

We uncovered a positive statistical correlation between the number of patents granted, the Global Innovation Index and the number of R&D FDI projects. Meaning that more innovative nations are more likely to receive R&D investments. We also identified the growing role of R&D investments as a proportion of total FDI.

2026 Outlook: R&D FDI will continue to account for more than 6.5% of global FDI projects but it is unlikely to grow further as many R&D projects are aligned with the software & IT services sector, which is struggling to grow.

SEPTEMBER

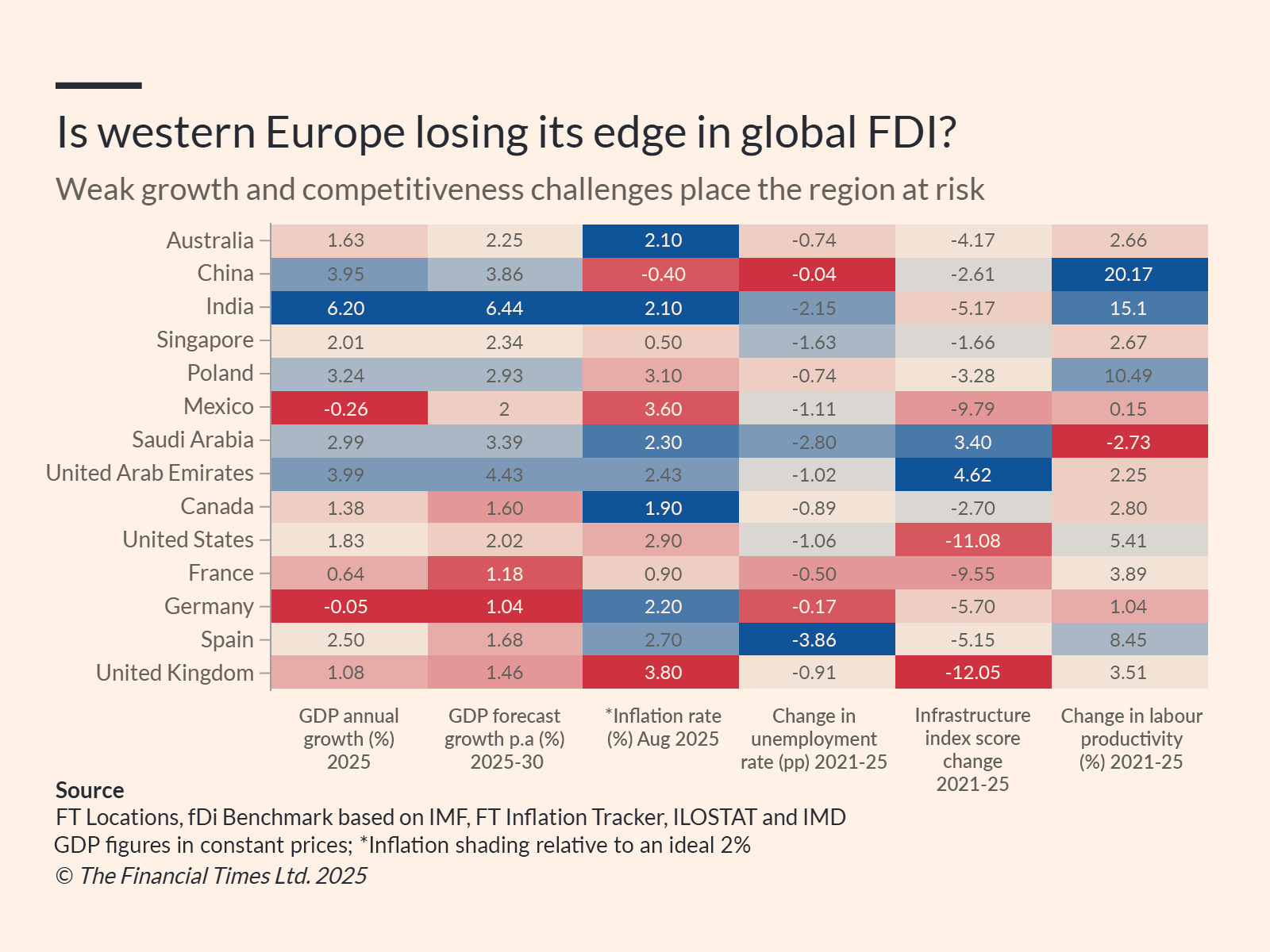

Western Europe’s FDI struggle continues

Although western Europe remains the leading destination region for FDI, its appeal is waning. In 2024, although global FDI activity rose, it declined into western Europe. The region’s struggles are continuing in 2025 and another decline in FDI project activity (for the third consecutive year) looks very likely. We assessed western European countries’ competitiveness against key competitors and found that low economic growth, slow productivity gains, a sticky labour market and required infrastructure improvements as well as dealing with the aftermath of unusually high inflation has caused investor concern. Strong policy decisions and improvements in innovation may well be key to turning around the region’s fortunes.

2026 Outlook: The required policy changes to improve western Europe’s appeal are unlikely to change in the short term. Yet, many countries are focusing on emerging tech and cleantech sectors. Innovation in these areas could once again see western Europe posting positive growth numbers, however a bottoming out of its current decline is the more likely optimistic view.

Western Europe losing its edge in global FDI across multiple indicators

OCTOBER

Data centre investments hit record highs

Capital investment in data centre FDI in 2025 has already exceeded the full-year total for 2024, with data to September showing a marked increase in spending, even as the number of projects remains steady. The jump is largely driven by large-scale investments from major tech firms.

Companies such as AWS, Google, Fir Hills, Brookfield Asset Management, Evroc and MGX Fund Management have each announced data centre projects worth over $1bn abroad in 2025. Many are also recipients of significant incentive packages, particularly in the US, according to data from our IncentivesFlow database. The average size of data centre projects has grown sharply, rising from $191m in 2016 to $855m this year — underscoring how data infrastructure is becoming an increasingly capital-intensive play.

2026 Outlook: Data centres will remain a key area of focus for many companies. They are the infrastructure needed to power the future technologies, with artificial intelligence, cloud and quantum computing examples of key reliance industries. The opportunity for FDI to play a key role in data centre development is clear. A continued upward trend is likely in 2026, with opportunities for more activity in emerging markets.

NOVEMBER

Is China’s dominance slowing electric vehicle FDI activity?

Foreign direct investment in electric vehicles has declined since 2023, following a strong run of growth from 2016 to 2022. Our analysis suggests China’s dominance in both EV supply and demand may be reshaping global FDI patterns. China now accounts for 65% of global EV sales, but demand in other key markets — notably Europe and North America is weakening. A mix of reduced policy support, rising tariffs, high vehicle prices, and cost of living pressures are weighing on growth. Infrastructure gaps, such as limited charging networks, have further dampened consumer demand.

While much of China’s EV strength is domestically driven, its companies are increasingly pursuing regional manufacturing strategies abroad. Despite heightened scrutiny of outbound Chinese investment, we’ve tracked several major projects in 2025 — including Sunwoda’s $1bn battery plant in Thailand and BYD’s $280m headquarters and R&D facility in Hungary.

Electric vehicle sales are increasing across major markets in 2025

2026 Outlook: The direction of FDI in 2026 will hinge largely on policy decisions — both those aimed at attracting EV-related projects and broader stances towards China’s role in the global EV market, from vehicle sales to component exports. On the demand side, factors such as affordability and infrastructure will remain critical. The short-term outlook is cautious, but investment levels are expected to pick up towards the end of the decade, especially as countries push to meet 2030 climate and industrial goals. Inbound FDI is likely to be led by the US and Europe, where industrial strategies and green transition funding are key drivers. Outbound flows will continue to rely heavily on Asian firms, particularly from China, India, Japan and South Korea.

Overarching FDI trend in 2025

FDI project activity is forecast to decline by between 4% and 8.5% in 2025. US tariffs have prompted many companies to delay decisions, marking a clear shift in investor sentiment. Combined with the lagged effects of a weaker macroeconomic environment in recent years, this is likely to result in the first drop in project numbers since 2020.

The outlook for 2026 remains muted. However, while tariffs are typically seen as a drag on globalisation, they may prompt some firms to redirect investment — either by establishing operations in the US to avoid the charges, or by diversifying production elsewhere to reduce reliance on the American market.

All analysis in the data trends emails are driven by data from fDi Markets, fDi Benchmark, IncentivesFlow, with additional insights from fDi Strategies.

Stay up to date with the latest data trends by signing up to our Knowledge Hub to receive our fortnightly email which samples a preview of exclusive insights. Sign up now

Further reading

Track global investment signals and trends with fDi Markets

Benchmark against your competitors with fDi Benchmark

Track incentives deals and policies using IncentivesFlow

Get expert strategy and consultancy advice from fDi Strategies

Learn more about FT Locations

FT Locations is the world's most comprehensive and trusted provider of investment promotion and economic development data and digital solutions for the foreign and domestic direct investment industry.